1. Stay Committed, but Stay Sharp

Whether you’re building wealth for retirement, children’s education, or financial independence, stick to your investment strategy. Review it annually to ensure you’re still aligned with your goals, time horizon, and risk profile. Every few years, conduct a deeper portfolio review to identify whether you need to recalibrate for performance or changing life circumstances.

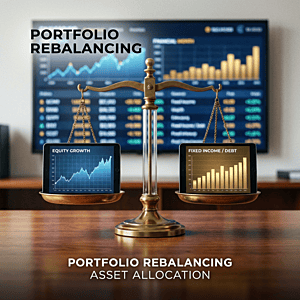

2. Rebalance to Protect Growth

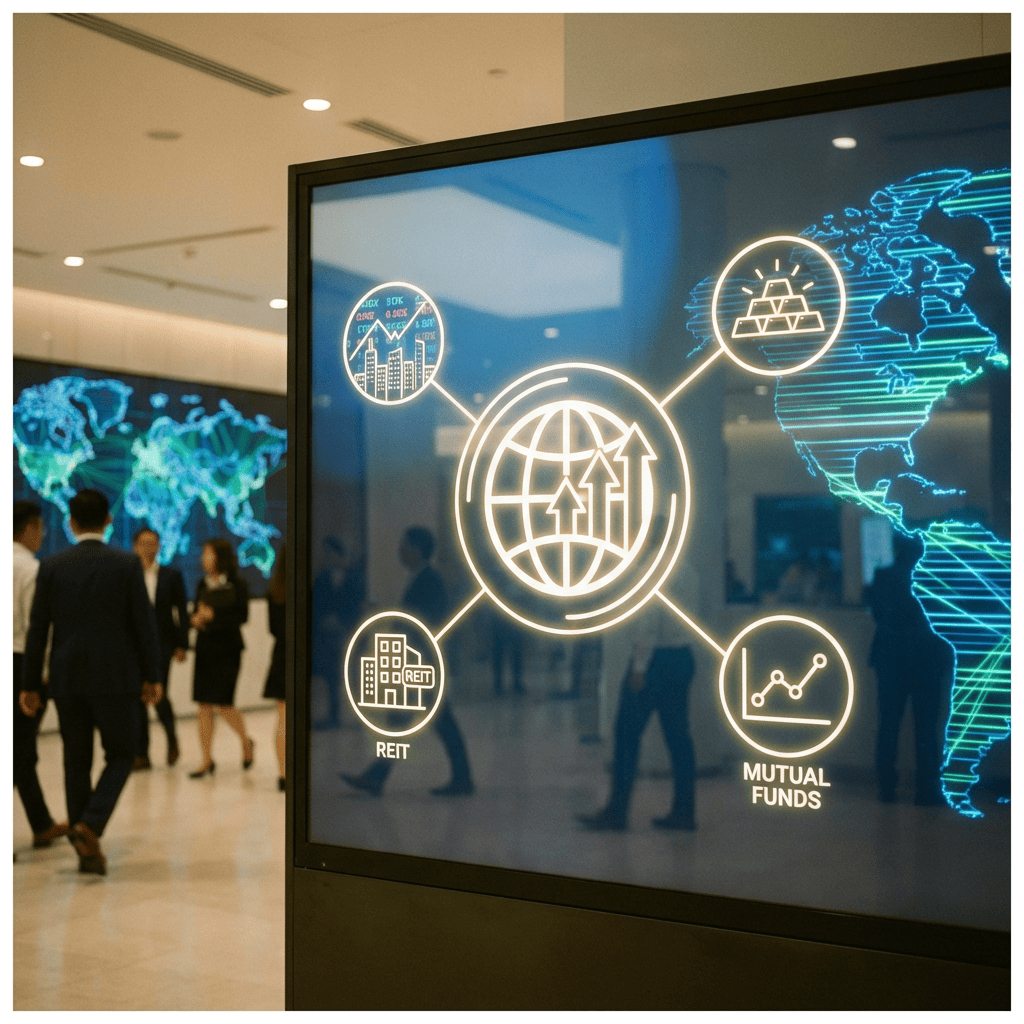

3. Expand and Diversify

- Sector diversification: Balance across domestic equities, international markets, and emerging sectors.

- Asset-class expansion: Explore REITs, gold, or select hybrid funds to stabilize returns.

- Goal-linked SIPs: Continue systematic investing, but with goal-specific targeting (e.g., education fund SIPs, wealth creation SIPs).

4. Optimize for Tax Efficiency

- ELSS or NPS for deductions. (as applicable from time to time based on allowed exceptions)

- Long-term capital gains optimization by staggering redemptions.

- Tax-efficient switching between funds instead of unplanned withdrawals.

- Tax planning during the grow phase ensures more compounding power remains in your hands.

5. Keep Emotions Out of Investing

When markets soar, greed tempts you to chase returns; when they fall, fear pushes you to exit. Both hurt compounding. The grow phase rewards those who hold steady, invest regularly, and avoid reactionary decisions. Automated SIPs or STPs help maintain emotional discipline.

6. Prepare for Transition

As you approach key life or financial milestones, begin shifting gradually from aggressive to moderate instruments. This allows you to lock in gains and prepare for the Preserve Phase without sudden shocks.